NCLT Chennai-1 (2025.05.30) in Kannan Sambasivam Vs. A V K Raja & Ors. [IA(IBC)/1777 (CHE)/ 2023 in IBA/355/2020] held that;

That a mere suspicion upon the correctness of the invoice produced by an importer is not sufficient to reject it as evidence of the value of imported goods. The doubt held by the officer concerned has to be based on some material evidence and is not to be formed on a mere suspicion or speculation.

We may hasten to add that although strict rules of evidence do not apply to adjudication proceedings under the Act, yet the Adjudicating Authority has to examine the probative value of the documents on which reliance is sought to be placed by the revenue.

It is well settled that the onus to prove undervaluation is on the revenue and once the revenue discharges the burden of proof by producing contemporaneous imports at an evidence of higher price, the onus shifts to the importer to establish that the price indicated in the invoice relied upon by him is correct.

The asset purchase agreement between the beneficiary company and the CD is of dated 16.10.2019 is after the date of resignation, i.e 14.08.2019, of Respondent 4 and 5. Thus, on the date of alleged undervalued transaction, the Respondent 4 and 5 were not the directors of the CD. So, the CD and the beneficiary company cannot be held as related party.

In the present case, the CIRP commenced on 28.01.2021 and the alleged undervalued transaction was made on 16.10.2019, which was more than one year preceding the commencement of CIRP. It is already held that, the CD and the beneficiary company are not the related parties. That being the position, the alleged undervalue transaction would fall beyond the look back period of one year.

Based on the above findings and in the absence of the actual market value of the assets that were sold, this Tribunal holds that the liquidator has not provided sufficient proof to show that the impugned transaction has not taken place in the ordinary course of business of the CD. We are of the view that the impugned transaction does not meet the requirements of Section 45(2) to hold it as an undervalued transaction.

Excerpts of the order;

# 1. This is an application filed by the liquidator seeking the following reliefs:

a. To declare the transactions as Under Valued Transactions which have been carried on with the intent to defraud the creditors of the corporate debtor, under the section 45 of the Insolvency and Bankruptcy Code, 2016 and make respondents liable to such contribution to the assets of the corporate debtor as it may deem fit and

b. To direct the respondents to return the amount of Rs.18.87 Crores, to the Liquidation estate of the corporate debtor and

c. To pass such other orders as it deems fit in the above circumstances of the case and thus render justice.

# 2. It is stated that on an application filed under Section 7 of the Insolvency and Bankruptcy Code, 2016 ("Code") against Kapico Motors India Private Limited (hereinafter referred to as "Corporate Debtor"), this Tribunal passed an order in IBA/355/2020 dated 28.01.2021, initiating CIRP against the Corporate Debtor and appointed the Applicant, Kannan Sambasivam as the Interim Resolution Professional (In brevity IRP) to carry out the functions mentioned under the Code.

# 3. It is stated that, since no Resolution plan was received during the CIRP period, the COC passed a resolution to liquidate the corporate debtor. Accordingly the resolution professional filed an application seeking liquidation of the corporate debtor. The tribunal passed an order for Liquidation of the corporate debtor in IA/324/2022 in IBA/355/2020 dated 28.04.2022 and appointed the Applicant herein as the Liquidator.

# 4. It is stated that, on scrutinizing the books of accounts for the financial years 2018-2019, 2019-2020 and 2020-2021, the applicant observed lot of financial deviations. The applicant conducted the 3rd Committee of the Creditors Meeting(CoC) on 4th Dec 2021 and brought to knowledge of the COC members about the financial deviations noticed in the books of accounts of the corporate debtor. It is stated that COC authorized the Applicant to appoint an auditor to conduct the Transaction audit of the books of accounts of the corporate debtor.

# 5. It is stated that, the applicant on 24.07.2021 appointed M/s QED Corporate Advisors LLP, to conduct the transaction audit to cover the PUFE transactions under Sections 43, 45, 50 and 66 of the IBC 2016. 6. It is stated that, the M/s QED Corporate Advisors LLP conducted the transaction audit of the financial statements for the FY 2017-18, FY 2018-19, FY 2019-20 and provisional unaudited statement of the FY 2020-21 and also te Tally ERP back for the period 01-04-2017 to 31-3-2020 (audited) and for the period 01-04-2020 to 31-03-2021 (unaudited) and submitted the Transaction Audit Report on 22.03.2023.

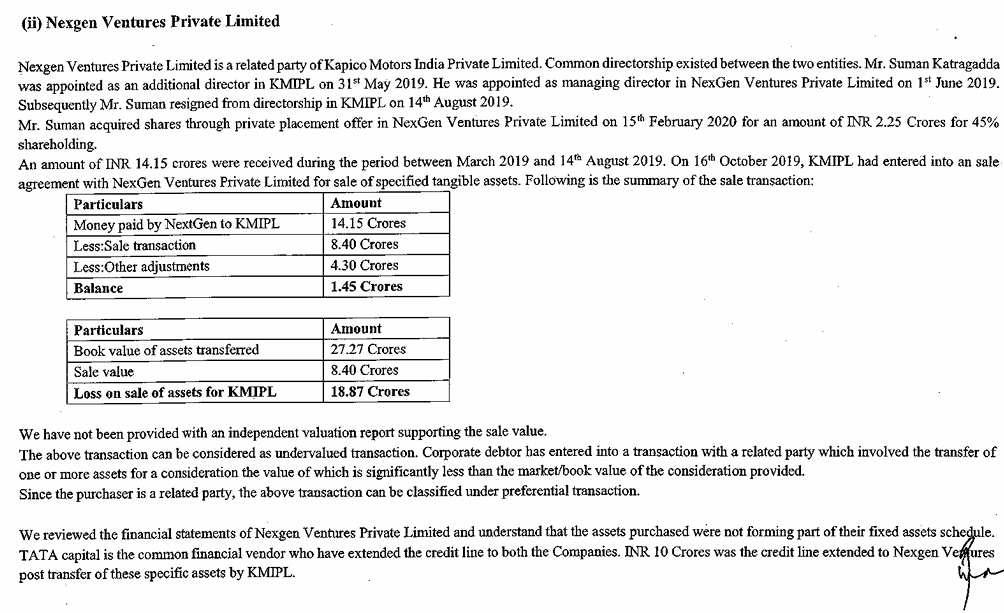

# 7. It is stated that, the Executive Summary of the Transaction Audit (4) (ii) reveals that the corporate debtor carried out an Undervalued Transaction to one of its related party company Nexgen Ventures Private Limited (hereinafter referred as beneficiary/nexgen) during the financial year 2019- 2020 qua the sale of the assets of the corporate debtor causing loss to the tune of Rs.18.87 Crores. The summary of the asset’s sale transactions is extracted below:

For the Financial Year 2019-2020:

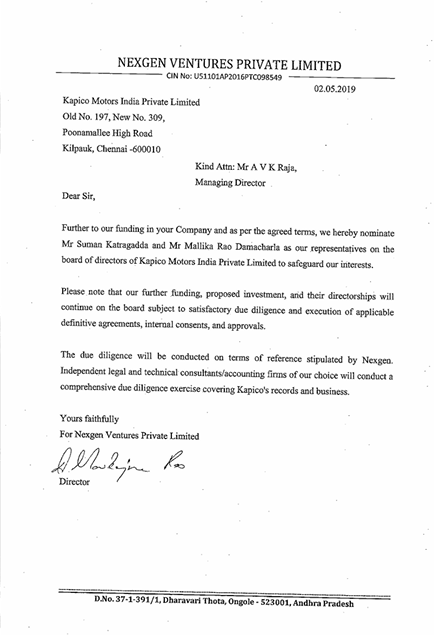

# 8. It is stated that, the 4th Respondent Mr. Suman Katragadda, who is currently one of the directors of the Nexgen Ventures Private Limited had joined as director in the board of the corporate debtor on 31/05/2019 and resigned from the board on 14/08/2019, He joined as director with the beneficiary company Nexgen Ventures Private limited on 01/06/2019.

# 9. It is stated that, 5th Respondent Mr. Mallikarjuna Rao Damacharla, who is currently the director in the Nexgen Ventures Private Limited, also joined as director in the board of the corporate debtor on 31/05/2019 and resigned on 14/08/2019. The Respondent No.5 was already on the board of the Nexgen Ventures Private limited as director since 17/03/2016 (As per MCA record). Form No DIR-12 for the appointment of R4 and R5 as the directors of the corporate debtor is enclosed as Annexure 4 and Form No DIR-12 qua resignation of the respondents R4 and R5 as directors of the corporate debtor is enclosed as Annexure 5.

# 10. It is stated that, the Corporate Debtor on 16/10/2019 had signed an Asset Purchase Agreement with the beneficiary for the sale of the assets of the corporate debtor to the value of Rs.8.40 Crores. The details of the corporate debtor's assets sold is given in the Annexure of the agreement. The agreement was signed on behalf of the corporate debtor by Mr. A V K Raja, Managing Director of the Corporate debtor and on behalf of the beneficiary by Mr. Mallikarjuna Rao Damacharla, the Managing Director of the beneficiary company.

# # 11. It is stated that, the details of the Fixed Assets as on 01/04/2019 and 31/03/2020 are enclosed as Annexure 7. The total value of the fixed assets as on 01/04/2019 is Rs.28.19 Crores and the total value of the fixed assets as on 31/03/2020 is Rs.85.04 Lakhs. Accordingly, total value of the fixed assets eroded during the FY 2019-2020 to Rs.27.34 Crores but as per the Asset Purchase Agreement dated 16/10/2019 the said fixed assets mentioned in the agreement were sold only for Rs.8.40 Crores.

# 12. It is stated that on scrutinising the Journal Entries, it was observed that following entries were made in the books of accounts as Sales to the beneficiary:

# 13. The beneficiary Ledger Account Statement for the period from 1/04/2018 to 31/03/2023 is enclosed as Annexure 8. It is stated that the statement clearly states that all the financial transaction happened between the Corporate Debtor and the beneficiary company.

# 14. The bank statements of the corporate debtor with the State Bank of India for the period April 2019 to June 2019 and July 2019 to Sept 2019 are enclosed as Annexure 9 and Annexure 10 respectively. It is stated that the bank statements reveal that all the receivables and payment were made to the beneficiary company during the period April 2019 to Sept 2019.

# 15. It is stated that the applicant mailed the draft copy of the Transaction Audit Report to the erstwhile directors on 06/02/2023 and sought for their clarification (Copy of the mail is enclosed herewith as Annexure 11) and the erstwhile directors sent a reply on 2/3/2023 (copy of their reply is enclosed as part of the Transaction Audit Report - Annexure 3).

# 16. It is stated that, the Audited Balance Sheet as on 31/3/2019 mentioned the value of the Fixed Assets as Rs.28,19,12,505 and the Audited Balance Sheet as on 31/3/2020 mentioned the value of the Fixed Assets as Rs.85,04,167. Accordingly, the value of the Fixed Assets eroded by Rs.27,34,08,338 during the FY 2019-2020, however as per the Asset Purchase Agreement dated 16/10/2019, the said fixed assets were sold for Rs.8.40 Crores only. Hence the corporate debtor with clear intention to defraud the creditors sold the Fixed Assets of the corporate debtor to the loss of Rs. 18.87 Crores and this transaction is clearly an Undervalued Transaction carried out by the corporate debtor to benefit the beneficiary company, Nexgen Ventures Private Limited.

# 17. It is stated that, since their responses did not clarify the queries raised in the draft transaction audit report, he has filed the instant application seeking the suitable remedies.

# 18. It is stated that, the above transaction was carried out with an intention to defraud the creditors of the corporate debtor and could potentially be classified as Under Valued Transactions as per Section 45 of the Insolvency and Bankruptcy Code, 2016.

COUNTER AFFIDAVIT ON BEHALF OF THE RESPONDENTS NO. 1, 2&3

# 19. The Respondent 1,2 & 3 filed a common reply and stated that, the COC in the meeting held on 04.12.2021 approved the appointment of the Transaction Auditor, namely QED Corporate Advisors LLP. As per Sections 25(1), 43 to 51 and 66 of the Code, its mandate was to investigate Avoidable Transactions involving the Corporate Debtor. The Transaction Auditor submitted its Report on 22.03.2023, highlighting certain irregularities in the Corporate Debtor's transactions. Based on the report, the Liquidator has filed this Application without independent opinion u/s 45 of the I&B Code read with Rule 11 of the NCLT Rules, 2016. Notably, without an independent opinion, no application under Section 45 is tenable before this Tribunal.

# 20. It is stated that, in the executive summary of the Transaction Audit Report, the Corporate Debtor was alleged to have been involved in an undervalued transaction with a related party, Nexgen, during FY 2019-20. According to the report, this transaction led to a significant loss of Rs. 18.87 Crores, a "central issue" in this case.

# 21. It is stated that, the present application filed against the 5 erstwhile directors of the Corporate Debtor under Section 45 of the Insolvency and Bankruptcy Code, 2016 (I&B Code) is liable to be dismissed in limine being not maintainable as it seeks a relief which is not maintainable in law primarily on the following grounds:

a. This application is unsustainable due to non-joinder of proper parties and misjoinder of parties.

b. This application is unsustainable since the impugned transactions challenged therein were entered beyond the relevant period. It has been filed based on the misconceived fact that the beneficiary was related to the Corporate Debtor, alleging that the transaction was entered within the relevant period.

c. Claims are factually unsustainable because the transactions were not undervalued.

# 22. It is stated that, the application is liable to be dismissed because of nonjoinder of the necessary party, namely Nexgen Ventures Private Limited ("Nexgen" or "Beneficiary"), the beneficiary of the alleged undervalued transaction. This is a crucial legal argument that needs to be addressed. Further, the respondents have been wrongly and illegally arrayed as

respondents in the purported application.

# 23. It is stated that, the beneficiary was not a related party of the CD at any time, as alleged by the Applicant. The CD was in dire need of funds to meet various financial obligations, and therefore, it approached the beneficiary for funding, either in the form of an investment or a loan. Based on the arrangement, beneficiary provided financial support as and when the CD needed. The funding arrangement started in March 2019 and the funding was for Rs.14.15 Crores. The Board resolution of the CD to avail loan from the beneficiary for 20 crores is extracted here below:

# 24. It is stated that, because of the said funding and to evince interest, beneficiary company nominated 4th and 5th Respondents as Directors of the CD w.e.f 31.05.2019 to ascertain the CD business's viability to take a call on investment and further funding. After considering the non-viability of the company's business, R4 and R5 resigned as Directors of the Company w.e.f 14.08.2019 within 3 months from the date of their appointment. It is stated that, they were never involved in the affairs of the CD. It is stated that R4, R5 and beneficiary never had any shareholding in the CD. The letter dated 02.05.2019 from the beneficiary appointing Respondent 4 & 5 is extracted below.

# 25. It is stated that, the Respondents wish to emphasise that neither R4 & R5 nor the beneficiary were related to the CD at any time. However, the Applicant misconstruced that the R4 and R5 were related to the Corporate Debtor: The above facts prove that R4, R5 and the Beneficiary were not associated with the CD as related party covered under any of the provisions of IBC. The relationship between them and CD was purely a Creditor-Debtor relationship; therefore, R4, R5 and Beneficiary were unrelated parties to the CD.

# 26. It is stated that, the funds received from the Beneficiary were utilised primarily to discharge the dues of the other financial creditors. It is stated that R1 settled the CD's significant dues from his sources and beneficiary; therefore, Nexgen became a vital lender of the CD. It is stated that R1 settled around Rs. 40 Crores with various financial creditors during pre-CIRP and post-CIRP. Therefore, no creditors lodged any claim with the Applicant during the liquidation period except GST Authorities and the PF department.

# 27. It is stated that, since CD's business was unviable, beneficiary expressed its unwillingness to support further funding or investment and conveyed that it wants to start dealership business independently, thereby sought repayment of the loan extended to the CD. The Respondents explored all possible ways to prevent further liabilities from being incurred. The Respondents made a full enquiry into the Company's affairs and formed an opinion that the CD continuing the operations would result in further liability, and keeping the assets would also incur colossal expenditures.

# 28. It is stated that, in this backdrop, beneficiary showed its interest in purchasing the impugned assets subject to valuations. The CD and the beneficiary appointed their valuers, and based on the valuation reports given by the valuers, the price was fixed. The assets were transferred in consideration of dues of Rs.8.40 crores payable to the beneficiary. R1 gave his assets as security for the remaining dues payable by CD to the beneficiary. (copy of the Valuation Report issued by the registered valuer is enclosed and marked as ANNEXURE-R/6, copy of the Memorandum of Deposit of Title Deeds executed by R1 in favour of Nexgen is enclosed and marked as ANNEXURE-R/7)

# 29. It is stated that for a transaction to come within Section 45 of the IBC, 2016:

(a) there must be a "transaction";

(b) it has taken place within the "relevant period" within the meaning of s 46; and

(c) it is an "undervalue" within the meaning of s 45 (2). In this case, the sale of the assets was a "transaction" that was entered on or about 16.10.2019, and CD was placed into CIRP on 28.01.2021.

# 30. It is stated that, beneficiary was not a related party to the CD, and any transactions within one year from the commencement date of CIRP, i.e., between 27.01.2020 and 28.01.2021, would be considered relevant. Moreover, as stated supra, R4 and R5 were the directors of the CD as nominated by Nexgen for only three months, from 31.05.2019 to 14.08.2019 and had mere debtor and creditor relationships not beyond that. In this case, the transaction was entered on 16.10.2019. i.e., beyond the "relevant period" and does not fall under Section 46 of the IBC, 2016.

# 31. It is stated that, the primary contention of the Applicant is that CD's fixed assets, as of 31.03.2019, having a book value of Rs. 28.19 Crores, were transferred to the beneficiary for Rs. 8.40 Crores on 16.10.2019, thereby it was an undervalued transaction that caused CD a loss of Rs. 18.87 Crores. In this connection, it is stated that the Book Value is not the correct measurement to ascertain the undervalued transactions covered under IBC, 2016. Book value is the net value of a CD's assets on its balance sheet, primarily based on the original acquisition cost of the respective assets after deduction of allowable depreciation. The market value of such assets would be based on their nature. If such assets are appreciable, the market value would be higher than the book value. If such assets are depreciable, the market value would be less than the book value. In the instant case, all assets were highly depreciable and not marketable.

# 32. It is stated that, to sell any assets, the Board of Directors, being commercial men, valued the assets only on a factual basis and not at cost or their value appearing in the books. It is stated that all the assets and liabilities must be taken at a fair value/market value, not merely at a book value. It is not always necessary to accept the book value. The actual test is to determine the fair value or the market value. The correct value is the market price or the cost price. The market price is more relevant since they were the used assets in this case. If the liquidator doubted the price at which the assets were sold, he should have ascertained the property's actual value. If the assets sold were less than the actual value, then the difference between the value arrived by the liquidator and the value of assets sold, should have been considered as undervalued. In this case, there was no such exercise on the part of the liquidator or the transaction auditor, and they relied on the value that appeared in the books.

# 33. It is stated that, the transaction auditor failed to understand the nature of assets sold and its marketability. Maruti Udyog Limited (MUL) had appointed the CD as an Authorised Dealer. To meet the criteria laid down by MUL, CD had to employ large number of staff to establish the showrooms and service stations as per MUL's mandate. The CD made huge investments and created fixed assets, including all showrooms in leased premises and maintained the showrooms spending crores of Rupees. The CD also raised loans worth crores of rupees from the banks and other financial lenders to fulfil the criteria and obligations laid down by the MUL. Due to heavy losses during 2019 on account of business crises, especially in the auto industry, the CD approached MUL to transfer the CD dealership to others to avoid further losses since maintenance of the showrooms and service stations involved huge expenses like rental, salary and other operating costs. It is stated that, the showrooms and service stations could not be used for any purpose other than the MUL dealership. It is stated that the CD duly apprised MUL of the reasons for heavy losses incurred by the CD vide its letter and email dated 26.07.2019 and 09.08.2019, respectively. (A copy of the letter and email dated 26.07.2019 and 09.08.2019 are enclosed and marked as ANNEXURE-R/8)

# 34. It is stated that, the sold assets comprised of 14 layouts structured according to specifications and design mandated by MUL. Though the book value of the assets is higher, they could not be sold by the CD without the concurrence of the MUL and there was no scope for purchase, by any parties other than the MUL dealers. Moreover, the transaction was based on the assessment and valuation made by the parties. The business loss was also duly claimed in the tax return filed for the relevant AY 2020-21, which the income tax department allowed. It is stated that, the sale consideration is driven by market forces, especially those willing to have a dealership similar to MUL. Further, current sale consideration was what a third-party buyer would be willing to pay based on proper valuation. Therefore, the same cannot be considered as undervalued transaction covered under the provisions of Section 49 of IBC. (A copy of the Tax Audit Report for the AY 2020-21 is enclosed and marked as ANNEXURE-R/10)

# 35. It is stated that, had the CD continued the business, it would have resulted in enormous future business losses. CD's decision to sell the showrooms and service stations in the ordinary business minimized any further losses due to CD's performance. It is stated that on these explanations, the Transaction Auditor and Liquidator should have considered and dropped the audit findings but, the transaction auditor observed mechanically and misconstrued that the transaction was undervalued.

# 36. It is stated that, assuming that the impugned transaction was entered within the relevant period without accepting the same, the only dispute is whether the Transactions were at an "undervalue" within s 45(2) of IBC, 2016. It is stated that the submission of the Applicant is that, the net book value of the assets, is significantly more than the sale value of the assets at the material time, however, there are no findings, opinions of the liquidator or the transaction auditor on the market value of the impugned assets at the material time.

# 37. It is stated that, assuming that the book value is an appropriate method to ascertain the actual value of the assets; then, valuation mandated under CIRP, or Liquidation becomes meaningless. For example, if a CD bought an immovable property for Rs. 10 Lakhs ten years back, it showed Rs. 10 lakhs as book value from the date of purchase to date, but it doesn't mean that the value of the said asset is still Rs.10 lakhs. The value of such assets would have been more than Rs. 10 Lakhs because immovable property is highly appreciable. This situation would be converse if the assets are depreciable, as in the instant case, the revalue of depreciable assets will depend upon usage, adaptability and market forces. It is stated that, though the book value of the impugned assets is higher, it is unsuitable for other car dealers, and only MUL dealers could use them. If any of the MUL dealers show no interest in buying the said assets, then the assets have no value at all. Under these circumstances, the CD had no alternative but to sell to Nexgen to settle their dues, which wanted to be the MUL dealer after getting proper valuations.

# 38. It is stated that, the Applicant's claim has no factual basis and Rs.8.40 Crores was provided by adjusting beneficiary’s financial debts for the Transaction. NexGen's consideration for the Transaction was not significantly less than the value of the assets since they were sold based on the valuation. Thus, the Transaction was not undervalue within Section 45 of IBC, 2016.

# 39. It is stated that, the Application contains no pleading of fact showing the impugned assets' market value at the material time. It relies upon the book value, which does not represent the fair market value or market value of the impugned assets at the material time. Therefore, the pleadings do not disclose a reasonable cause of action for a claim based on Section 45. Moreover, the impugned assets were sold in the ordinary course of business based on the proper valuation report. Hence, the contention that they are undervalued is factually and legally unsustainable.

# 40. It is stated that, the purported application is solely based on a misconceived Transaction Report with false allegations. The genesis between the beneficiary and the Corporate Debtor and the impugned transactions is missing in the purported application and the transaction audit report.

COMMON COUNTER STATEMENT OF THE 4TH & 5TH RESPONDENT

# 41. Respondent 4th and 5th have filed their common reply and stated that, the application is neither maintainable in law nor on fact. It is stated that the application has been filed with unexplained delay and laches and is barred by limitation:

# 42. It is stated that, CIRP of the Corporate Debtor commenced on 28.01.2021 and the present Application has been filed on 05.10.2023 without any pleading or explanation for the undue delay in preferring the same.

# 43. It is stated that, the Regulation 35A of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process for Corporate substituted Persons) Regulations, by Notification No. 2016 as IBBI/2018-19/GN/REG031, dated 3rd July, 2018 (w.e.f. 04-07-2018), provides the timelines within which preferential and other transactions are to be determined and filed by the RP. The said Regulation is also reiterated in Regulation 40A that deals with the model time-line for corporate insolvency resolution process. The Hon'ble Supreme Court in Arcelormittal India (P) Ltd. v. Satish Kumar Gupta (2019)2 SCC 1 has emphasized the significance of the model timelines as provided in Reg 40A and stated that they are to be followed as closely as possible by all the authorities. The Applicant has severely flouted the timelines prescribed and the same has been captured in the following table:

# 44. It is stated that, there is an unexplained delay of 845 days in preferring the Application and the Application is liable to be dismissed.

# 45. It is stated that, as per the statutory mandate of the Code read with Regulation 35A, the RP ought to have formed an opinion whether the CD had been subjected to any transactions covered u/s 43, 45, 50 or 66 within 75 days of commencement of CIRP. If such an opinion was formed, the RP ought to have made a determination of the same within 115 days and ought to have filed the Application within 135 days from commencement date. The pleadings and documents of the Application under reply reveal that no such opinion was formed, or determination was made prior to filing of the Application.

# 46. It is stated that, the Applicant failed to independently apply his mind and form an opinion or make a determination as mandated under law.

# 47. It is stated that, the NCLT Kolkata Jitendra Lohia vs. Nikhil Chowdhury and others [Ι.Α. (IB) No. 208/KB/2021INC.P (IB) No.204/KB/2019] has held as under:

"16. We have carefully seen the averments of the application and corresponding reply of the respondents. We have noticed that the allegations made in application do not constitute anything actionable against the respondents. It was the duty of the RP to come to conclusive determination before filing an application with the Adjudicating Authority. Simply by repeating the extracts or observations made in the forensic auditor's report, the RP could not make an independent determination about the nature of transactions as required by Regulation 35A (2) of the CIRP Regulations."

48. The NCLT Kolkata (30.06.2022) in Kshitiz Chhawchharia vs. Madhumalati Merchandise Private Limited & Ors [I.A. (IB) No. 346/KB/2019 In CP (IB) No. 349/KB/2017) held that:

"6.8. Further, Regulation 35A(3) of the CIRP Regulations provides that upon making such determination under regulation Resolution 35A(2), the Professional shall apply to the Adjudicating Authority for the appropriate relief on or before the one hundred and thirty-fifth day of the insolvency commencement date. In this case, the one hundred and thirty fifth day is on 23 May 2018. The instant application being IA. (IBC) 346/KB/2019 has been filed on 20 March 2019, thus making it clear that the Applicant has not complied with the provisions of regulation 35A within the timeline provided therein.

6.9. . . . . , we do not see any "determination" within the meaning of regulation 35A of the CIRP Regulations. Therefore, we will not act as court of first instance to determine the nature of the transactions mentioned hereinabove.

6.1 In light of the above facts and circumstances, the adjudicating Authority is satisfied that the instant application is not maintainable and the same is therefore rejected."

# 49. It is stated that, the Applicant has filed this Application on assumptions and presumptions and solely on the transaction audit report. In Para 18 of the application the Applicant states, that since the responses did not clarify the queries raised in the transaction audit in the draft report, he has filed this application seeking suitable remedies. It is stated that the notices appear to have been sent only to the 1st to 3rd Respondents and not the answering Respondents.

# 50. It is stated that, without issuing a notice or seeking explanation from the Respondents, conclusions have been made. Neither the transactional auditor nor the Applicant called upon the Respondents to tender explanation. It is stated that, the said findings and procedure adopted by the Applicant are in gross violation of the principles of natural justice and equity.

# 51. It is stated that, this application is liable to be dismissed on primary ground of non-joinder of M/s. Nexgen Ventures Pvt. Ltd. It is stated that Nexgen Ventures Pvt. Ltd. is the only beneficiary of the alleged undervalued transaction and hence, would be a necessary party, without which, the proceedings cannot sustain.

# 52. It is stated that the 4th and 5th Respondents have been wrongfully arrayed in their individual capacity as Respondents in the Application. The inclusion of 4th and 5th Respondents, who are not relevant to the alleged undervalued transaction, constitutes misjoinder of parties.

# 53. It is stated that, the relationship between the CD and Nexgen Ventures Pvt. Ltd. was purely that of creditor and debtor. They were not the related parties as per the provisions of the IBC. The CD had resolved to borrow a loan of Rs.20,00,00,000/- from Nexgen Ventures Pvt. Ltd. and to issue warrants and fully convertible debentures. Nexgen Ventures Pvt. Ltd. provided financial support to the CD and initially lent Rs.14.15 Crores. Similarly, Nexgen Ventures Pvt. Ltd. also passed resolutions to lend to the CD.

# 54. It is stated that, 4th and 5th Respondents who were Directors in. Nexgen Ventures Pvt. Ltd., were appointed as directors of the CD on 31.05.2019 upon the nomination of Nexgen Ventures Pvt. Ltd. to assess the business viability of the CD for further potential investment. They resigned on 14.08.2019 after determining that further investment was not viable. Apart

from that, they had no involvement in the CD's transactions or decision making or management. It is stated that neither the answering Respondents nor Nexgen Ventures Pvt. Ltd. held any shares in the CD.

# 55. It is stated that, since the CD business was found unviable, Nexgen Ventures Pvt. Ltd. demanded repayment of the loan advanced to the CD. It was thereafter that both the parties appointed independent valuers and decided to sell the assets to Nexgen Ventures Pvt. Ltd. at the price of Rs.8.40 crores. It is stated that the 1st Respondent had also pledged his personal property with Nexgen Ventures Pvt. Ltd. for the balance dues of the CD, Nexgen Ventures Pvt. Ltd. did not pursue any claim with the CD for the balance amount.

# 56. It is stated that, the impugned transaction occurred on 16.10.2019, whereas the CIRP commenced on 28.01.2021. As per Section 46 of the IBC, the relevant period for reviewing transactions is one year before the commencement of CIRP for unrelated parties. Since Nexgen Ventures Pvt. Ltd. was not a related party, transactions between 27.01.2020 and 28.01.2021 are relevant. The transaction therefore falls outside the look back period.

# 57. It is stated that, the Audit report has several disclaimers and limitations whereby it was categorically admitted and stated among others that

i) the findings cannot be taken to be exhaustive in view of the fact that only specific sample of transactions were reviewed and that it is possible that observations may have been different had the whole documentation/information were provided and reviewed on a particular matter;

ii) The understanding observations of the merely represents facts and possible interpretations and that clients are advised to take expert opinion before initiating action;

iii) We did not obtain third party confirmations directly from banks, vendors, customers, third parties, etc. for the transactions selected for review due to paucity of time, etc.

# 58. It is stated that, the Application has been filed invoking Section 45 the Code alleging undervalued transactions against the Respondents. It is well settled that in case such allegations are levelled, the burden of proving the same beyond reasonable doubt lies on the person levelling such allegations. In the present case, mere book entries cannot not prevail over the reports of the independent valuers.

# 59. The Hon'ble Supreme Court in Commissioner of Customs Vs. Aggarwal Industries Ltd.(2012)1 SCC 186 has held that a mere suspicion upon the correctness of the invoice produced by an importer is not sufficient to reject it as evidence of the value of imported goods. The doubt held by the officer concerned has to be based on some material evidence and is not to be formed on a mere suspicion or speculation. We may hasten to add that although strict rules of evidence do not apply to adjudication proceedings under the Act, yet the Adjudicating Authority has to examine the probative value of the documents on which reliance is sought to be placed by the revenue. It is well settled that the onus to prove undervaluation is on the revenue and once the revenue discharges the burden of proof by producing contemporaneous imports at an evidence of higher price, the onus shifts to the importer to establish that the price indicated in the invoice relied upon by him is correct.

FINDINGS AND OBSERVATIONS OF THIS TRIBUNAL

# 60. Heard the counsels for the parties and perused the documents.

# 61. It is the case of the liquidator that, the CD made an undervalued transaction by entering into an asset purchase agreement dated 16.10.2019 with the beneficiary company. The asset purchase agreement provides for sale of fixed assets of the CD and the total sale consideration was 8,40,00,000/- (Eight Crore Forty Lakhs Only). It is further the case of liquidator that, the audited balance sheet as on 31/03/2019 mentions the value of the fixed assets as Rs.28,19,12,505/- and the audited balance sheet as on 31/03/2020 mentions the value of the fixed assets as Rs.85,04,167/-(Eighty Fife Lakhs Four Thousand One Hundred Sixty Seven). Nonetheless, the asset purchase agreement signed between the CD and the beneficiary provides for the sale consideration to the tune of Rs.8.40 crores. Consequently, value of the fixed assets of the CD eroded to the extent of 18.87 crores.

# 62. The Liquidator appointed a transaction auditor, i.e., QED Corporate Advisors LLP, on 24.07.2021 to conduct the transaction audit of the CD. The transaction auditor subhmitted the final report on 22.03.2023 in which, the transaction auditor provided that, the transaction entered between the CD and the beneficiary company can be considered as an undervalued

transaction. The report also stated that, the beneficiary company is a related party to the CD as there were common directors in the companies. The extract of the report is provided here below:

# 63. The Respondent 1,2 and 3(suspended directors of CD) in their reply have stated that, the application is liable to be dismissed on the grounds of non-joinder of parties as the beneficiary company is not made as the party to the application. It was stated that, the CD and the beneficiary company are not the related parties and the application has been filed beyond the relevant period as provided in Section 46 of the Code. It was stated that, the nature of relation between the CD and the beneficiary is of creditor and debtor.

# 64. The Respondent 1,2 and 3 have stated that, the liquidator failed to consider the market value of the properties that were sold to the beneficiary company under the asset purchase agreement dated 16.10.2019. The liquidator only considered the book value and the same does not show the actual value of the properties that were sold. The liquidator also failed to ascertain the actual value. The transaction audit report as well also failed to consider the actual value of the assets that were sold.

# 65. The Respondent 4 and 5 (currently the directors of the beneficiary company) reiterated the contention of the Respondent 1,2 and 3 and stated that, the relationship between the CD and the beneficiary is that of creditor and debtor and they are not the related parties. The liquidator failed to ascertain the actual value and did not prove the allegation of undervalue transaction beyond reasonable doubt. It was stated that, the Respondent 4 and 5 were appointed as directors from 31.05.2019 till 14.08.2019 and the asset purchase agreement was entered between the CD and beneficiary on 16.10.2019. Thus, there was no related party transaction.

# 66. Upon perusing the factual matrix, the following issues arise;

a. Whether the beneficiary is a related party to the CD and alleged undervalue transaction between the CD and the beneficiary falls within the look back period of 2 years as per Section 46(1)(ii) of the Code?

b. If the findings of the first issue is in affirmative, whether the liquidator has provided sufficient proof to prove that the CD entered into a transaction for a consideration the value of which is significantly less that the value of the consideration provided by the CD and such transaction has not taken place in the ordinary course of business of the CD?

# 67. It is seen that, the CD had taken financial assistance form the beneficiary which is also evidenced in the ledger statement provided along with the application. The Respondent 4 and 5 were appointed as directors of CD on 31.05.2019. They resigned from CD on 14.08.2019. The respondents in their reply have annexed the letter dated 02.05.2019 from the beneficiary company addressed to the CD, which states that the Respondent 4 and 5 were nominated by the beneficiary company as the representatives on the board of directors of CD to analyse the business viability of the CD. The letter dated 31.05.2019 states that, the beneficiary company withdraws the proposed investment and asked Respondent 4 and 5 to resign from the board of CD with immediate effect.

# 68. The asset purchase agreement between the beneficiary company and the CD is of dated 16.10.2019 is after the date of resignation, i.e 14.08.2019, of Respondent 4 and 5. Thus, on the date of alleged undervalued transaction, the Respondent 4 and 5 were not the directors of the CD. So, the CD and the beneficiary company cannot be held as related party.

# 69. It is relevant to extract Section 46 of the Code, which provides as under;

46. Relevant period for avoidable transactions. –

(1) In an application for avoiding a transaction at undervalue, the liquidator or the resolution professional, as the case may be, shall demonstrate that –

(i) such transaction was made with any person within the period of one year preceding the insolvency commencement date; or

(ii) such transaction was made with a related party within the period of two years preceding the insolvency commencement date.

(2) The Adjudicating Authority may require an independent expert to assess evidence relating to the value of the transactions mentioned in this section.

# 70. The Section 46(1)(i) provides that, the liquidator must demonstrate that the undervalued transaction was made with any person within the period of one year preceding the date of commencement of CIRP. Section 46(1)(ii) provides that, in the case of related party, the transaction must have been made within two years preceding the date of commencement of CIRP. In the present case, the CIRP commenced on 28.01.2021 and the alleged undervalued transaction was made on 16.10.2019, which was more than one year preceding the commencement of CIRP. It is already held that, the CD and the beneficiary company are not the related parties. That being the position, the alleged undervalue transaction would fall beyond the look back period of one year.

# 71. The Section 45 provides as under;

45. Avoidance of undervalued transactions. –

(1) If the liquidator or the resolution professional, as the case may be, on an examination of the transactions of the corporate debtor referred to in subsection

(2) 1[***] determines that certain transactions were made during the relevant period under section 46, which were undervalued, he shall make an application to the Adjudicating Authority to declare such transactions as void and reverse the effect of such transaction in accordance with this Chapter.

(2) A transaction shall be considered undervalued where the corporate debtor–

(a) makes a gift to a person; or

b) enters into a transaction with a person which involves the transfer of one or more assets by the corporate debtor for a consideration the value of which is significantly less than the value of the consideration provided by the corporate debtor, and such transaction has not taken place in the ordinary course of business of the corporate debtor.

# 72. As per Section 45 (2) of the Code, a transaction is considered to be undervalued when the Corporate Debtor either makes a gift to a person or enters into a transaction with a person which involves the transfer of one or more assets by the Corporate Debtor for a consideration, the value of which is significantly less than the value of the consideration provided by the Corporate Debtor, and such transaction has not taken place in the ordinary course of business of the Corporate Debtor.

# 73. In the present case, the audited financial statement as on 31.03.2019 provides the fixed assets value to be 28,19,12,505/-(Twenty Eight Crore Nineteen Lakhs Twelve Thousand Five Hundred Five Rupees), whereas, the audited financial statements as on 31.03.2022 provides the fixed assets value to be Rs. 85,04,167/- (Eighty Five lakhs Four Thousand One Hundred and Sixty Seven Thousand Rupees). The difference in the fixed assets value is around 27.27 crores and the sale consideration as per the assets purchase agreement between CD and the beneficiary is 8.40 crores. In the transaction audit report, the market value of the assets sold was not given. Further, there are no findings, opinions or pleadings of the liquidator on the market value of the impugned assets at the material time. We find substance in the contention of the Respondents that the book value is not the correct measurement to ascertain the undervalue transactions. The book value is the net value of the Corporate Debtor assets on its balance sheet primarily based on the original acquisition cost of the assets after deduction of allowable depreciation. Market value of such assets would be based on their nature. If the assets are appreciable, the market value would be higher than the book value and if the assets are depreciable, the market value would be less. In the instant case, the Corporate Debtor was appointed as the authorized dealer of Maruti Udyog Limited(MUL). It made huge investments and created fixed assets including showrooms. It raised the loans to create infrastructure for the showrooms. It suffered heavy losses due to business crisis in auto industries. This led to contact the beneficiary namely Nexgen. As per the agreement with MoU, the showrooms and service stations could not be used for any purpose other than specified by MoU. Although the book value of the assets were higher but the assets could not be sold without the concurrence of the MUL. There was no scope for purchase by any parties other than MUL dealers. The sale consideration was driven by market forces specially those willing to have a dealership. The beneficiary showed its interest and the parties appointed the valuers to arrive at the market value of the assets. Nothing can be made out from the above that the Corporate Debtor did the undervalue transactions with the beneficiary company Nexgen to drive benefit out of it rather the said transactions were made with Nexgen, not being the related party in the ordinary course of business to come out of the rigors of heavy losses suffered by the Corporate Debtor.

3 74. The Respondents in their reply have attached the valuation report.

a. The valuation report attached by the Respondent No 1,2 & 3 provides the valuation of the assets of CD as Rs.8,00,89,093/-. The report is extracted here below;

b. The valuation report attached by the Respondent No 4 & 5 dated 20.09.2019 provides the valuation of the assets of CD as Rs.8,14,28,921/-. The report is extracted here below

# 75. Based on the above findings and in the absence of the actual market value of the assets that were sold, this Tribunal holds that the liquidator has not provided sufficient proof to show that the impugned transaction has not taken place in the ordinary course of business of the CD. We are of the view that the impugned transaction does not meet the requirements of Section 45(2) to hold it as an undervalued transaction.

# 76. In the light of above discussions, we do not find any merits in the application qua declaring the transactions as undervalue transactions which have been carried on with an intent to defraud the creditors or to make the Respondents liable to such contributions to the assets or to direct the Respondents to return an amount of Rs. 18.87 Crores to the liquidation estate of the Corporate Debtor as prayed for.

# 77. We accordingly dismiss the application with no orders as to cost.

-------------------------------------------

No comments:

Post a Comment